via @marketsmarkets The global medical image management market is expected to reach USD 5.78 Billion by 2021 from USD 4.22 Billion in 2016, growing at a CAGR of 6.5% from 2016 to 2021. The factors driving market growth include technological advancements in diagnostic imaging modalities and image management solutions, growing investments in the medical imaging market, government initiatives to encourage EMR adoption, increasing usage of imaging equipment, rapid growth in geriatric imaging volumes, growing adoption of VNA, growing adoption of image management systems by small hospitals and imaging centers and rapidly growing big data in healthcare. Furthermore, the integration of PACS/VNA with EMR and ECM and increasing consolidation in healthcare have opened an array of opportunities for the growth of the medical image management market.

However, factors such as longer product lifecycle of VNAs and budgetary constraints may restrain the market growth.

Medical image management is a process of electronically managing medical images with the help of image management systems. These systems control, manage, and store medical imaging data along with other patient information in a healthcare system. Picture archiving and communication systems (PACS), vendor-neutral archives (VNA), and application-independent clinical archives (AICA) are the three major technologies used in image management systems.

On the basis of product, the medical image management market is segmented into Picture Archiving and Communication System (PACS), Vendor Neutral Archive (VNA), and Application Independent Clinical Archive (AICA). The PACS segment is estimated to command the largest share in 2016 as it is the oldest and pioneering technology in this market. Apart from this, some other factors contributing to its large share include growing volume of imaging procedures, technological advancements in PACS, and adoption of the PACS in new imaging segments such as endoscopy, ophthalmology, mammography, and oncology. On the basis of end user, the medical image management market is segmented into hospitals, diagnostic imaging centers, and other end users (Ambulatory surgical clinics, small clinics and contract research organizations).

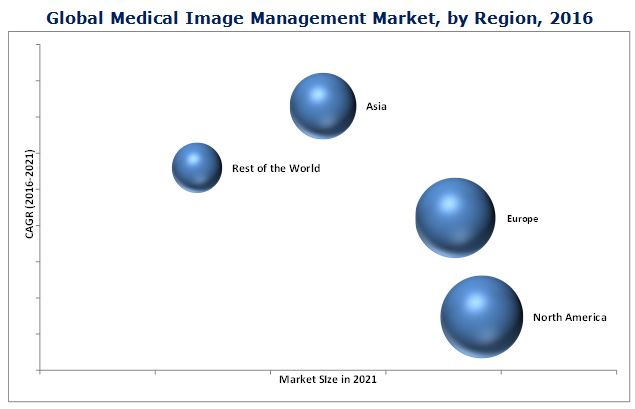

North America dominates the medical image management market, with the U.S. accounting for the major share. This can be attributed to the increase in the geriatric population, high incidence/prevalence of various diseases (such as cancer and CVD), the large number of imaging centers in this region, ongoing research activities, fast adoption of technologically advanced imaging systems, and increasing awareness about the benefits of early diagnosis of diseases.

The prominent players in the medical image management market are McKesson Corporation (U.S.), GE Company (U.S.), Fujifilm Holdings Corporation (Japan), Merge Healthcare Inc. (IBM Corporation) (U.S.), Agfa-Gevaert Group (Belgium), Philips Healthcare (Royal Philips Electronics)(The Netherlands), Siemens Healthcare (Siemens AG)(Germany), Carestream Health, Inc. (Onex Corporation) (U.S.), BridgeHead Software (U.K.), and Novarad Corporation (U.S.).

Market Stakeholders:

- Medical image management software providers

- Diagnostic imaging equipment vendors/service providers

- Standalone image management software/workstation providers

- Healthcare IT service providers

- Research and consulting firms

- Diagnostic imaging centers

- Hospitals

- Venture capitalists

- Government agencies

- Market research and consulting firms

Scope of the Report

The research report categorizes the medical image management market into the following segments and subsegments:

- Medical Image Management Market, by Product

- Picture Archiving and Communication Systems (PACS)

- PACS Market, by Type

- Departmental PACS

- Departmental PACS Market, by Type

- Radiology PACS

- Cardiology PACS

- Other Departmental PACS

- Enterprise PACS

- PACS Market, by Type

- Vendor Neutral Archives (VNA)

- VNA Market, by Type

- On-premise

- Hybrid VNA

- Cloud-based VNA

- VNA Market, by Procurement Model

- Departmental VNA

- Multidepartment VNA

- Multisite VNA

- VNA Market, by Type of Vendor

- PACS Vendors

- Independent Software Vendors

- Infrastructure/Storage Vendors

- VNA Market, by Type

- Application-independent Clinical Archives (AICA)

- AICA Market, by Type of Vendor

- VNA Vendors

- Native AICA Vendors

- AICA Market, by Type of Vendor

- Picture Archiving and Communication Systems (PACS)

- Medical Image Management Market, by End User

- Hospitals

- Diagnostic Imaging Centers

- Other End Users (ambulatory surgical centers, small clinics, and contract research organizations)

- Medical Image Management Market, by Region

- North America

- U.S.

- Canada

- Europe

- Germany

- U.K.

- France

- Italy

- Spain

- Rest of Europe (RoE)

- Asia

- Japan

- China

- India

- Rest of Asia (RoA)

- Rest of the World (RoW)

- North America